![]()

100% Updated CIMA CIMAPRA19-F03-1 Enterprise PDF Dumps

Use Valid Exam CIMAPRA19-F03-1 by DumpsTorrent Books For Free Website

CIMA F3 Certification Exam is a challenging and rewarding exam that offers finance professionals the opportunity to develop their skills and knowledge in financial strategy. It is a valuable certification that can enhance career prospects and open up new opportunities in the finance industry.

NEW QUESTION # 245

A listed company is considering either a one-off special divided or a share repurchase scheme to reduce its surplus cash level.

Identify TWO advantages that a one-off special payment has over a share repurchase scheme.

- A. It will reduce the possibility of a hostile takeholder

- B. It allows shareholder a choice of option in or out of the payment.

- C. It would result in a transfer of wealth back to the shareholder

- D. It will change balance of share owners.

- E. It is easier to arrange than a share repurchase

Answer: C,E

Explanation:

Compared with a share repurchase, a one-off special dividend:

is administratively simpler to arrange,

returns surplus cash directly to shareholders (all shareholders receive cash, ownership proportions are unchanged).

Answers: D and E

NEW QUESTION # 246

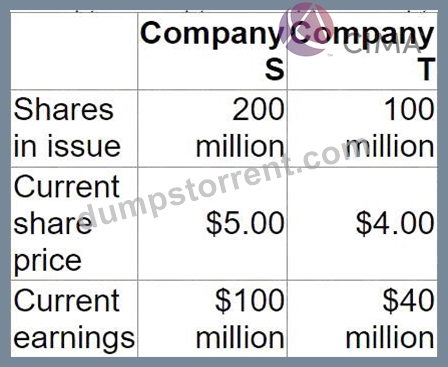

Company S is planning to acquire Company T.

The shareholders in Company T will receive new shares in Company S in an all-share consideration.

Relevant information:

The shareholders in Company T want sufficient shares to receive a 25% premium on the pre-acquisition value of their shares, based on the pre-acquisition share price.

Which of the following share-for-share offers will achieve the desired result?

- A. 1 share in Company S for 2 shares in Company T

- B. 2 shares in Company S for 1 share in Company T

- C. 10 shares in Company S for 4 shares in Company T

- D. 1 share in Company S for 1 share in Company T

Answer: D

Explanation:

The pre-acquisition share prices are:

Company S: $5.00

Company T: $4.00

Shareholders in Company T want a 25% premium on the value of their shares, based on T's current price:

Required value per T share=4.00×1.25=$5.00\text{Required value per T share} = 4.00 \times 1.25 = \$5.00 Required value per T share=4.00×1.25=$5.00 Now value each offer using Company S's pre-acquisition share price of $5:

A). 2 S shares for 1 T share

Value received = 2×5=$102 \times 5 = \$102×5=$10 # 150% premium (too high)

B). 1 S share for 1 T share

Value received = 1×5=$51 \times 5 = \$51×5=$5 #

Premium =5#44=25%= \frac{5 - 4}{4} = 25\%=45#4=25% #

C). 1 S share for 2 T shares

That's 0.5 S per T # 0.5×5=$2.500.5 \times 5 = \$2.500.5×5=$2.50 # actually a discount

D). 10 S shares for 4 T shares

That's 2.5 S per T # 2.5×5=$12.502.5 \times 5 = \$12.502.5×5=$12.50 # huge premium (>200%) Only offer B gives T's shareholders exactly a 25% premium.

Correct answer: B - 1 share in Company S for 1 share in Company T.

NEW QUESTION # 247

WW is a quoted manufacturing company. The Finance Director has addressed the shareholders during WW's annual general meeting-She has told the shareholders that WW raised equity during the year and used the funds to repay a large loan that was maturing, thereby reducing WW's gearing ratio At the conclusion of the Finance Director's speech one of the shareholders complained that it had been foolish for WW to have used equity to repay debt The shareholder argued that the Modigliani and Miller model (with tax) offers proof that debt is cheaper than equity when companies pay tax on their profits.

Which THREE arguments could the Finance Director have used in response to the shareholder?

- A. A lower gearing ratio creates greater flexibility for WW in the future

- B. A lower gearing ratio will result in an increase in the value of the company

- C. WW was approaching a debt covenant limit and it was therefore important to reduce gearing.

- D. Reducing the gearing ratio has reduced the financial risk of WW which will benefit shareholders

- E. The Modigliani and Miller model would only be valid in practice if WW's shareholders were aware of the model and believed in its validity

- F. The shareholder was confusing the cost of capital with shareholder wealth

Answer: B,C,D

NEW QUESTION # 248

A company's dividend policy is to pay out 50% of its earnings.

Its most recent earnings per share was $0.50, and it has just paid a dividend per share of $0.25.

Currently, dividends are forecast to grow at 2% each year in perpetuity and the cost of equity is 10.5%.

In order to grow its earnings and dividends, the company is considering undertaking a new investment funded entirely by debt finance. If the investment is undertaken:

* Its cost of equity will immediately increase to 12% due to the increased finance risk.

* Its earnings and dividends will immediately commence growing at 4% each year in perpetuity.

Which of the following is the expected percentage change in the share price if the new investment is undertaken?

- A. Increase = 8.3%

- B. Increase = 2%

- C. Increase = 10.5%

- D. Decrease = 7.7%

Answer: A

Explanation:

Current:

DPS just paid D0=0.25D_0 = 0.25D0=0.25, growth g = 2%, ke=10.5%k_e = 10.5\%ke=10.5% D1=0.25×1.02=0.255,P0=0.2550.105#0.02=0.2550.085=3.00D_1 = 0.25 × 1.02 = 0.255,\quad P_0 = \frac

{0.255}{0.105 - 0.02} = \frac{0.255}{0.085} = 3.00D1=0.25×1.02=0.255,P0=0.105#0.020.255=0.0850.255=3.00

After investment: growth g = 4%, ke=12%k_e = 12\%ke=12%

D1#=0.25×1.04=0.26,P1=0.260.12#0.04=0.260.08=3.25D_1' = 0.25 × 1.04 = 0.26,\quad P_1 = \frac{0.26}

{0.12 - 0.04} = \frac{0.26}{0.08} = 3.25D1#=0.25×1.04=0.26,P1=0.12#0.040.26=0.080.26=3.25 Percentage change:

3.25#3.003.00=0.253=8.33%\frac{3.25 - 3.00}{3.00} = \frac{0.25}{3} = 8.33\%3.003.25#3.00=30.25=8.33%

NEW QUESTION # 249

Which of the following statements are true with regard to interest rate swaps?

Select ALL that apply.

- A. When interest rates are falling the risk of default by the fixed interest rate payer is low.

- B. An nicest rate swap is an internal hedging technique.

- C. Some companies interest rate swap to deliberately increase their risks because they believe that they are better at predicting future interest rates than the market.

- D. An interest rate swap is an external hedging technique.

- E. Risk of default is high from the floating interest rate payer if interest rates rise.

Answer: C,D

Explanation:

Interest rate swaps are covered in CIMA F3 under risk management and derivative instruments, specifically as tools for managing interest rate risk. An interest rate swap is an agreement between two parties to exchange interest payment obligations, typically swapping fixed-rate interest payments for floating-rate payments, or vice versa, on a notional principal amount.

Option A is TRUE.

CIMA F3 recognises that although swaps are primarily used for hedging, some companies may enter into interest rate swaps for speculative or risk-taking purposes. If management believes it has superior forecasts of future interest rate movements compared to the market, it may deliberately increase exposure to interest rate risk by swapping into floating rates or fixed rates accordingly. This behaviour is discussed in F3 as speculation rather than pure hedging.

Option E is TRUE.

An interest rate swap is an external hedging technique. CIMA F3 clearly distinguishes between:

Internal hedging (e.g. matching assets and liabilities, netting, leading and lagging), and External hedging, which involves using financial instruments with third parties, such as forwards, futures, options and swaps.

Since a swap involves a counterparty (often a bank or financial institution), it is classified as an external hedge.

The remaining options are incorrect:

B is FALSE. Default risk does not automatically become "high" for the floating-rate payer when interest rates rise; it depends on the firm's overall financial strength and cash flows. Rising rates increase payments, but not necessarily default risk to a high level.

C is FALSE. When interest rates fall, the fixed-rate payer is at a disadvantage (paying above-market rates), which may increase rather than reduce financial strain.

D is FALSE. An interest rate swap is not an internal hedging technique; it requires an external counterparty.

NEW QUESTION # 250

A company has a financial objective of maintaining a gearing ratio of between 30% and 40%, where gearing is defined as debt/equity at market values.

The company has been affected by a recent economic downturn leading to a shortage of liquidity and a fall in the share price during 20X1.

On 31 December 20X1 the company was funded by:

* Share capital of 4 million $1 shares trading at $4.0 per share.

* Debt of $7 million floating rate borrowings.

The directors plan to raise $2 million additional borrowings in order to improve liquidity.

They expect this to reassure investors about the company's liquidity position and result in a rise in the share price to $4.2 per share.

Is the planned increase in borrowings expected to help the company meet its gearing objective?

- A. No, gearing would increase and the gearing objective would be met before the announcement but exceeded after the announcement.

- B. No, gearing would increase and the gearing objective would be exceeded both before and after the announcement.

- C. Yes, gearing would fall and the gearing objective would be exceeded before the announcement but met after the announcement.

- D. No, gearing would increase but the gearing objective would be met both before and after the announcement.

Answer: B

Explanation:

Before announcement:

Equity = 4m shares × $4.0 = $16m

Debt = $7m

Gearing = 7 / 16 = 43.75% # already above 40%.

After additional $2m debt and higher share price:

Debt = 7 + 2 = $9m

Equity = 4m × $4.2 = $16.8m

Gearing = 9 / 16.8 # 53.6% # even further above the 40% ceiling.

So the gearing objective is exceeded both before and after, and gearing rises.

NEW QUESTION # 251

Company T is a listed company in the retail sector.

Its current profit before interest and taxation is $5 million.

This level of profit is forecast to be maintainable in future.

Company T has a 10% corporate bond in issue with a nominal value of $10 million.

This currently trades at 90% of its nominal value.

Corporate tax is paid at 20%.

The following information is available:

Which of the following is a reasonable expectation of the equity value in the event of an attempted takeover?

- A. $50.2 million

- B. $65.0 million

- C. $32.0 million

- D. $41.6 million

Answer: D

NEW QUESTION # 252

A company is preparing an integrated report according to the International <IR> Framework as issued by the International Integrated Reporting Council.

Which THREE of the following should be included in the report?

- A. A summary of the key issues discussed by directors in main board meetings.

- B. A comparison of the key elements of its financial statements with those of its main competitor.

- C. The challenges and uncertainties that the organisation is likely to encounter in pursuing its strategy.

- D. A detailed analysis of the organisation's business model.

- E. An explanation of how the organisation's governance structure supports its ability to create value in the short, medium and long term.

Answer: C,D,E

Explanation:

Integrated reports under the <IR> Framework should include:

Governance and how it supports value creation # A

The organisation's business model # B

Risks, challenges, and uncertainties affecting strategy and value creation # C Comparisons with competitors' financials (D) and a summary of board meeting discussions (E) are not required content elements in the <IR> Framework.

NEW QUESTION # 253

A company is currently all-equity financed with a cost of equity of 8%.

It plans to raise debt with a pre-tax cost of 4% in order to buy back equity shares.

After the buy-back, the debt-to-equity ratio at market values will be 1 to 2.

The corporate income tax rate is 30%.

Which of the following represents the company's cost of equity after the buy-back according to Modigliani and Miller's Theory of Capital Structure with taxes?

- A. 9.8%

- B. 9.4%

- C. 8%

- D. 13.6%

Answer: B

NEW QUESTION # 254

Which THREE of the following long term changes are most likely to increase the credit rating of a company?

- A. An increase in the interest cover ratio.

- B. An increase in the free cashflow generated from operations.

- C. A decrease in the (Net debt) / (Earnings before interest, tax, depreciation and amortisation) ratio.

- D. A decrease in the dividend cover ratio.

- E. A decrease in the (Book value of debt) / (Book value of equity) ratio.

Answer: A,B,C

Explanation:

We're looking for long-term changes that would improve a company's credit rating (i.e. reduce perceived credit risk and increase capacity to service debt):

A). Increase in interest cover (EBIT / interest) # higher coverage, safer for lenders # positive.

B). Decrease in (Net debt)/(EBITDA) # lower leverage relative to earnings # positive.

C). Increase in free cash flow from operations # more internally generated cash to pay interest and repay debt # positive.

D). Decrease in (Book debt)/(Book equity) is also a good sign in reality, but the question restricts us to three; exam focus is usually on coverage and cash flow-based ratios, so A, B and C are the best three.

E). Decrease in dividend cover (earnings / dividend) means paying a larger proportion of earnings out as dividends # less retained profit and weaker protection for creditors # negative for credit rating.

So the three most likely to improve the rating: A, B, C.

NEW QUESTION # 255

A company's latest accounts show profit after tax of $20.0 million, after deducting interest of $5.0 million. The company expects earnings to grow at 5% per annum indefinitely.

The company has estimated its cost of equity at 12%, which is included in the company WACC of 10%.

Assuming that profit after tax is equivalent to cash flows, what is the value of the equity capital?

Give your answer to the nearest $ million.

$ ? million

Answer:

Explanation:

300,

300000000

NEW QUESTION # 256

A listed publishing company owns a subsidiary company whose business activity is training.

It wishes to dispose of the subsidiary company.

The following information is available:

The board of the publishing company believe that the value of the subsidiary company, and hence the value of the equity invested in it, can be determined by calculating the present value of the subsidiary's free cashflows.

Which of the following is the most appropriate discount rate to use when determining the enterprise value of the company?

- A. A cost of equity that reflects the asset beta of a listed company that provides training activities.

- B. A WACC that reflects the gearing of the subsidiary company and the asset beta of a listed company that provides training activities.

- C. A WACC that the reflects the gearing of the publishing company and the equity beta factor of the publishing company.

- D. A WACC that reflects the gearing of the publishing company and the asset beta of a listed company that provides training activities.

Answer: B

Explanation:

Comprehensive and Detailed Step by Step Explanation with all CIMA F3: Financial Strategy documents: = When valuing a business by discounting free cash flows to the firm (FCFF), CIMA F3 explains that the correct discount rate is the weighted average cost of capital (WACC) of that specific business, not the parent's WACC. FCFF are cash flows available to both debt and equity providers, so they must be discounted using a rate that blends the required returns of debt and equity in proportion to the company's own capital structure.

The subsidiary operates in training, a different line of business from the publishing parent, so its business risk is better represented by the asset beta of a comparable listed training company. F3 teaches that you should use a sector asset beta to capture operating risk, then apply the gearing (debt-to-equity mix) of the business being valued to derive an appropriate WACC. Because the intention is to dispose of the subsidiary as a stand-alone entity, the relevant gearing is that of the subsidiary, not the publishing group.

Option C is therefore correct: it uses a WACC (appropriate for FCFF), based on the subsidiary's capital structure (financial risk) and the training-sector asset beta (business risk). Options A and D wrongly use the parent's gearing, and B uses only a cost of equity rather than WACC, so they are inconsistent with F3 valuation principles.

NEW QUESTION # 257

A listed company with a growing share price plans to finance a four-year research project with debt.

The main criterion for the finance is to minimise the annual cashflow payments on the debt.

The research will be sold at the end of the project.

Which of the following would be the most suitable financing method for the company?

- A. Bonds with warrants

- B. Finance lease

- C. Standard bonds

- D. Bank loan

Answer: A

NEW QUESTION # 258

Companies L. M N and O:

* are based in a country that uses the RS as its currency

* have an objective to grow operating profit year on year

* have the same total levels of revenue and cost

* trade with companies or individuals in the United States. All import and export trade with companies or individuals in the United States is priced in US$.

Typical import/export trade for each company in a year are as follows:

Which company's growth objective is most sensitive to a movement in the USS / RS exchange rate?

- A. Company L

- B. Company O

- C. Company N

- D. Company M

Answer: D

Explanation:

Imports and exports are in US$, home currency is RS. Each company has the same total revenue/cost level; what differs is their net US$ exposure, which drives how sensitive profit growth is to the US$/RS rate.

From the table:

Company L: Imports 10, Exports 20 # net export +10 US$m

Company M: Imports 0, Exports 18 # net export +18 US$m

Company N: Imports 25, Exports 21 # net import #4 US$m

Company O: Imports 15, Exports 0 # net import #15 US$m

Sensitivity to exchange rate = size of the net US$ position (absolute value).

Comparing: |+10|, |+18|, |#4|, |#15| # the largest is 18 for Company M.

So Company M's operating profit growth is most sensitive to movements in the US$/RS rate.

NEW QUESTION # 259

Company C is a listed company. It is currently considering the acquisition of Company D. The original founder of Company C currently owns 52% of the shares.

Alternative forms of consideration for Company D being considered are as follows:

* Cash payment, financed by new borrowing

* issue of new shares in Company C

Which of the following is an advantage of a cash offer over a share-for exchange from the viewpoint of the original founder of Company C?

- A. A share-for-share exchange would require the approval of the Competition Authorities but a cash offer would not.

- B. A share-for-share exchange would require the approval shareholders in Company C but a cash offer would not.

- C. A share for share exchange would result in a significant change in control of Company C whereas a cash offer would not.

- D. A cash offer would result in a lower gearing ratio therefore reduce the weighted overage cost of capital whereas a cash offer would not.

Answer: C

Explanation:

Founder of Company C owns 52% and wants to keep control.

A share-for-share exchange means issuing new shares # dilutes the founder's holding and may reduce control.

A cash offer financed by borrowing does not issue new shares # founder's percentage holding (and control) is preserved.

That is exactly what option A states.

NEW QUESTION # 260

The International Integrated Reporting Council (IIRC) was formed in August 2010 and brings together a cross-section of representatives from a wide variety of business sectors.

The primary purpose of the IIRC's framework is to help enable an organsation to communicate how it:

- A. contributes positively to the economic well being of the environment in which it operates.

- B. ensures that the conflicting needs of different stakeholder groups are met in an optimal manner.

- C. creates value in the short, medium and long term.

- D. minimises the environmental impact of its business processes.

Answer: C

NEW QUESTION # 261

Company T is a listed company in the retail sector.

Its current profit before interest and taxation is $5 million.

This level of profit is forecast to be maintainable in future.

Company T has a 10% corporate bond in issue with a nominal value of $10 million.

This currently trades at 90% of its nominal value.

Corporate tax is paid at 20%.

The following information is available:

Which of the following is a reasonable expectation of the equity value in the event of an attempted takeover?

- A. $50.2 million

- B. $65.0 million

- C. $32.0 million

- D. $41.6 million

Answer: D

Explanation:

In CIMA F3, equity valuation using P/E multiples is based on earnings available to ordinary shareholders (i.e.

profit after interest and tax). The syllabus emphasises that when valuing a potential takeover target, you should (1) derive maintainable post-tax earnings and then (2) apply a P/E multiple that reflects prices actually paid in comparable acquisitions, not just average stock-market multiples.

Calculate maintainable earnings:

Profit before interest and tax (PBIT) = $5m

Less interest on 10% bonds: 10% × $10m = $1m

Profit before tax = $4m

Tax at 20% = $0.8m

Earnings for equity = $3.2m

Select the appropriate P/E multiple:

F3 explains that "takeover P/Es" are usually higher than sector trading P/Es, reflecting the control premium.

Here we have:

Overall market P/E = 20

Retail sector P/E = 10

Recent retail takeovers P/E = 13

For a takeover valuation we use the 13× multiple from recent sector takeovers.

Compute equity value:

Equity value=3.2m×13=41.6m\text{Equity value} = 3.2\text{m} \times 13 = 41.6\text{m}Equity value=3.

2m×13=41.6m

Debt's market value (90% of $10m) is not added here because the P/E method already gives the equity value.

So, a reasonable expected equity value in a takeover is $41.6 million.

NEW QUESTION # 262

Company Z has just completed the all-cash acquisition of Company A.

Both companies operate in the advertising industry.

The market considered the acquisition a positive strategic move by Company Z.

Which THREE of the following will the shareholders of Company Z expect the company's directors to prioritise following the acquisition?

- A. The retention of key customers of the acquired company.

- B. The regulatory approval required to complete the acquisition.

- C. The integration and retention of key employees.

- D. The development of a dividend policy to meet the expectations of the target company shareholders.

- E. The realisation of anticipated post-acquisition synergies.

Answer: A,C,E

Explanation:

Reasoning:

After an all-cash acquisition which the market views positively, shareholders in Company Z will mainly focus on value delivery from the deal:

A). Realisation of anticipated synergies - core reason for doing the deal.

C). Integration and retention of key employees - critical in an advertising business where human capital and client relationships are key.

E). Retention of key customers of the acquired company - losing major clients would quickly destroy acquisition value.

B is not a priority: target company shareholders have already been paid out in cash.

D is irrelevant now: the acquisition has already been completed, so regulatory approval is in the past.

NEW QUESTION # 263

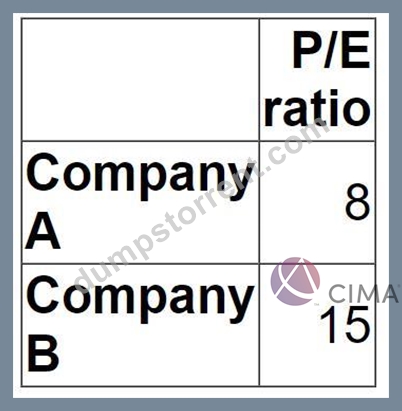

Two companies that operate in the same industry have different Price/Earnings (P/E) ratios as follows:

Which of the following is the most likely explanation of the different P/E ratios?

- A. Company B has higher business risk than Company A.

- B. Company B has a greater profit this year than Company A.

- C. Company B has higher gearing than Company A.

- D. Company B has higher expected future growth than Company A.

Answer: D

NEW QUESTION # 264

A company's gearing is well below its optimal level and therefore it is considering implementing a share re-purchase programme.

This programme will be funded from the proceeds of a planned new long-term bond issue.

Its financial projections show no change to next year's expected earnings.

As a result, the company plans to pay the same total dividend in future years.

If the share re-purchase is implemented, which THREE of the following measures are most likely to decrease?

- A. The interest cover

- B. The gearing, based on book value (debt ÷ (debt + equity))

- C. Next year's dividend per share

- D. The number of shares in issue

- E. The cost of equity

- F. The Weighted Average Cost of Capital

Answer: A,D,F

NEW QUESTION # 265

ZZZ wishes to borrow at a floating rate and has been told that it can use swaps to reduce the effective interest rate it pays. ZZZ can borrow floating at the risk-free rate + 1, and fixed at 10%.

Which of the following companies would be the most appropriate for ZZZ to enter into a swap with?

- A. Company AAB - it can borrow floating at risk-free rate + % and fixed at 9.5%

- B. Company DDA - it can borrow at risk-free rate + 1 Vz and fixed at 10.5%

- C. Company BBA - it can borrow floating at risk-free rate +VA and fixed at 12%

- D. Company CCA - it can borrow at risk-free rate + Y% and fixed at 9%

Answer: C

Explanation:

Against DDA

Fixed: ZZZ 10% vs DDA 10.5% # ZZZ cheaper by 0.5%

Floating: ZZZ rf+1 vs DDA rf+1.5 # ZZZ cheaper by 0.5%

ZZZ is better in both markets by the same margin # no comparative advantage, little reason for DDA to swap.

Against CCA

Fixed: ZZZ 10% vs CCA 9% # CCA cheaper by 1%

Floating: ZZZ rf+1 vs CCA rf+0.5 # CCA cheaper by 0.5%

CCA is cheaper in both, and also the one with greater advantage is fixed. There's no natural "ZZZ better at one, CCA better at the other" pairing.

Against BBA #

Fixed: ZZZ 10% vs BBA 12% # ZZZ cheaper in fixed by 2%

Floating: ZZZ rf+1 vs BBA rf+0.25 # BBA cheaper in floating by 0.75%

So ZZZ has an advantage in fixed, BBA has an advantage in floating.

ZZZ wants floating, so it can:

Borrow fixed at 10% (where it is strong),

Enter a swap with BBA (who wants fixed but is strong in floating),

End up with an effective floating rate below rf+1.

Against AAB

Fixed: ZZZ 10% vs AAB 9.5% # AAB cheaper by 0.5%

Floating: ZZZ rf+1 vs AAB rf+0.75 # AAB cheaper by 0.25%

AAB is cheaper in both; no obvious mutual gain.

So the classical swap pairing is ZZZ with BBA # Option C.

NEW QUESTION # 266

A company based in the USA has a substantial fixed rate borrowing at an interest rate of 3.5% and wishes to swap a part of this to a floating rate to take advantage of reducing interest rates Its bank has quoted swap rates of 3 4%-3 5% against 12-month USD risk-free rate.

What is the overall interest rate achieved by the company under this borrowing plus swap combination?

- A. 12-month USD risk-free rate minus 0 1 % (where 0 1 % = the fixed rate of 3.6% minus the swap rate of

3 4%) - B. 12-month USD risk-free rate

- C. 12-month USD risk-free rate plus 0 1% (where 0.1 % = the fixed rate of 3.5% minus the swap rate of 3

4%) D. Unchanged at 3.60% as this is the same as the swap rate

Answer: C

Explanation:

Company pays 3.5% fixed on its borrowing and enters a swap at 3.4-3.5% vs 12-month USD risk-free rate.

To move from fixed to floating, it will receive fixed 3.4% and pay floating (risk-free):

Net interest:

3.5%#3.4%+rf=rf+0.1%3.5\% - 3.4\% + \text{rf} = \text{rf} + 0.1\%3.5%#3.4%+rf=rf+0.1% Answer to Q102: C - 12-month USD risk-free rate plus 0.1%

NEW QUESTION # 267

Company ABC's management has noticed that Company BCD has quickly built up a 20% stake by buying shares in Company ABC and are concerned that this is the start of a hostile bid.

This build-up of shares triggers the poison pill provision which automatically converts the rights to buy future preference shares previously issued to existing shareholders in Company ABC to full ordinary shares

What is the most likely impact of the triggering of a poison pill strategy at this stage in the bidding process?

- A. Company ABC becomes less attractive due to a fall in value of the shares as a result of the discount.

- B. Company BCD loses value on its shareholding and has to sell at a loss before losing more value

- C. It is too late for a poison pill strategy to have any impact on a hostile takeover because Company BCD has already built up a significant stake in Company ABC.

- D. The threat of a hostile takeover is reduced because Company ABC becomes more expensive to buy.

Answer: D

NEW QUESTION # 268

A company has an opportunity to invest in a positive net present value project, but the project would require debt finance that would push the company's gearing ever a limit imposed by a debt covenant on an existing loan.

Which THREE of the following actions could be taken by the company?

- A. The directors could meet with key shareholder to discuss whether they wish the project proceed despite the breach of the covenant

- B. The company could seek alternative sources of finding, such as a reduction in the annual dividend payment, to finance the project.

- C. The project could be foregone if it cannot be funded without breaching the covenant

- D. The directors could proceed will the project because their primary duly is maximise shared older wealth, even if that conflicts with lenders' interest.

- E. The company could approach its existing Lenders to negotiate a relaxation of :he conditions imposed by the covenant.

- F. The project could proceed if the cash inflows from the project will enable some of the debt to be repaid before the end of the financial year and so the breach of covenant may never be detected

Answer: B,C,E

Explanation:

Acceptable actions:

Negotiate with lenders (A)

Drop the project if funding would breach the covenant (B)

Look for other finance such as cutting dividends (D)

Breaching covenants deliberately or relying on shareholders to "approve" a breach is not acceptable.

NEW QUESTION # 269

XYZ has a variable rate loan of $200 million on which it is paying interest of Liber ' 3%.

XYZ entered into a swap with AG bank to convert this to a fixed rate 8% loan. AB bank charges an annual commission of 0.4% for making this arrangement Calculate the net payment from KYZ to AB bank at the end of the first year if Libor was 2% throughout the year.

Give your answer in $ million, to one decimal place.

Answer:

Explanation:

22.8

NEW QUESTION # 270

......

CIMA CIMAPRA19-F03-1 Official Cert Guide PDF: https://guidetorrent.dumpstorrent.com/CIMAPRA19-F03-1-exam-prep.html